As automotive finance portfolios grow, contact centre cost becomes a structural constraint on profitability. Every agreement generates predictable servicing interactions such as settlement quotes, balloon repayment queries and account updates, all of which traditionally require agent time. As volumes increase, so do recruitment costs, training overhead, infrastructure demands and operational complexity. For many regulated lenders,

Author: Kevin Phillips

With portfolios growing year-on-year and customer expectations at an all-time high, automotive finance providers face a clear choice: scale costly contact centre operations or invest in digital self-service channels that delight customers and transform the bottom line.

The automotive finance sector is in the midst of a profound shift. Customers who arrange a Personal Contract Purchase, Hire Purchase, or lease agreement today expect the same seamless digital experience they receive from their bank, insurer, or broadband provider. They want instant access to their agreement data, frictionless tools to manage their finance, and the freedom to act without ever picking up the phone.

For finance providers, the opportunity is substantial. A well-executed digital self-service strategy delivered through a mobile app and supporting web portal, does not simply reduce operational cost. It builds lasting customer loyalty, creates new revenue opportunities, and future-proofs the business against the rising costs of increasing the number of in-life portfolios.

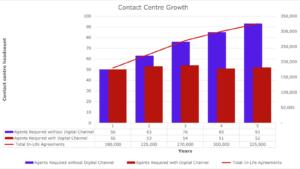

The Scale of the Challenge

Consider a mid-sized automotive finance provider with 150,000 active in-life agreements. At a typical contact rate, this portfolio generates tens of thousands of inbound calls, emails, and web enquiries every month — the vast majority of which are entirely routine: “What is my current outstanding balance?”, “Have I exceeded my mileage allowance?”, “What happens at the end of my agreement?” and “I need a quote for a

settlement figure.” These are precisely the interactions that digital self-service channels handle at a fraction of the cost and with vastly superior speed.

With the portfolio growing at 15% per year, the challenge compounds rapidly. By the end of Year 3, the same provider will be managing more than 228,000 agreements. Without a credible self-service strategy, meeting that demand requires proportional headcount growth in the contact centre — a costly, slow, and ultimately unsustainable response.

The Financial Case: £1.2 Million in Net Savings

The business case for digital self-service is compelling and measurable. The primary driver of cost reduction is deflection — moving routine enquiries away from the contact centre and into a channel that costs a fraction of the price to serve. When a customer retrieves a settlement quote digitally rather than calling an agent, the cost differential is typically between £4 and £8 per interaction. At scale, these savings accumulate rapidly.

Avoiding the need to hire additional contact centre agents as the portfolio grows is equally significant. Each full-time equivalent agent represents not just salary, but recruitment, training, management overhead, technology, and workspace costs. Holding headcount flat while the portfolio expands by 15% annually represents a material saving in its own right.

How a digital self-service engagement channel negates contact centre headcount increase

With many years experience and data modelling our automotive finance clients we have designed a digital banking experience specifically aligned with the needs of customers. The results are clear: the number of digital self-serve interactions keep pace with the growth of the finance organisation as they grow, allowing the contact centre to maintain size and handle only the more complex and situation-specific queries.

These figures are conservative. They do not account for the revenue uplift generated by digital end-of-term conversion, nor the reduced cost of complaint handling that accompanies a more transparent, proactive customer experience. The real return is higher still.

“Holding headcount flat while a portfolio grows by 15% annually is not merely a cost saving — it is a strategic advantage that compounds with every passing year.”

The Customer Experience: Clarity, Control, and Confidence

The most effective self-service channels are not simply digital replicas of paper statements. They are purpose-built experiences that give customers genuine clarity over their agreement and genuine control over their financial decisions. Done well, they transform a commodity product into a relationship.

AGREEMENT DASHBOARD

From the moment a customer logs in, they are greeted with a clean, personalised view of their in-life agreement. Monthly payment, next payment date, total amount of credit, term remaining, and annual mileage allowance are all presented clearly and in plain language. There is no need to search through a welcome pack or navigate an automated phone menu. The information a customer needs is immediate, accurate, and available at any time of day.

SETTLEMENT QUOTES ON DEMAND

One of the high volume, most routine enquiries in any automotive finance contact centre is the settlement quote. A customer considering a part-exchange, an early repayment, or a change in their financial circumstances needs to know their current settlement figure — and they need it quickly. Digital self-service delivers this instantly, with full transparency on how the figure is calculated, any early repayment adjustments, and the date until which the quote remains valid. The customer is empowered to make an informed decision without any agent involvement.

MILEAGE CALCULATOR

Mileage anxiety is one of the most common sources of customer concern in PCP and leasing agreements. A built-in mileage calculator allows customers to enter their current odometer reading and instantly see whether they are on track, over-contracted, or under-contracted against their agreed annual allowance. Where a customer is trending towards an excess mileage charge at the end of the term, the tool can surface options — such as purchasing additional mileage or adjusting driving behaviour — well in advance of the point of concern. This proactive transparency dramatically reduces end-of-term disputes and the associated cost of resolution.

END-OF-TERM BALLOON REFINANCE

The end of a PCP agreement represents a pivotal moment in the customer relationship — and a significant revenue opportunity. Customers who have received an outstanding digital experience throughout their in-life journey are substantially more likely to remain with the same provider. A digital self-service channel can surface a personalised balloon refinance offer in the weeks and months before term-end, allowing customers to subscribe to a new loan product without agent intervention. The conversion journey — from notification to application to approval — can be completed entirely digitally, reducing friction and increasing take-up rates.

Building Loyalty Through Digital Engagement

Customer loyalty in automotive finance is not built in the showroom, it is built during the three years of in-life agreement management that follows. A customer who feels informed, in control, and well-served throughout their agreement term is far more likely to return for their next vehicle. A customer who has experienced friction, confusion, or difficulty accessing basic information, is not.

Digital self-service delivers the conditions for loyalty to flourish. Proactive notifications — a payment reminder, a mileage alert, an end-of-term prompt — demonstrate that the finance provider is engaged and attentive. Transparent tools that demystify settlement figures and mileage positions build trust. A seamless refinance journey at term-end closes the loop and starts the next agreement on a foundation of positive experience.

→ 24/7 Availability — Customers access their agreement information outside of business hours, eliminating a major source of frustration.

→ Reduced Waiting Times — Routine enquiries that previously required a call are resolved in seconds, with no hold time.

→ Greater Transparency — Clear, plain-language presentation of agreement data reduces misunderstanding and complaint.

→ Proactive Communication — Automated alerts keep customers informed at key moments without requiring agent involvement.

→ Seamless End-of-Term Journey — Digital refinance subscription increases retention and lifetime customer value.

Mobile and Web: A Dual-Channel Strategy

The most successful implementations deliver self-service capability across both a dedicated mobile application and a responsive web portal. These channels serve different moments in the customer journey. The mobile application excels at immediacy: a quick mileage check, a payment confirmation, a notification about a quote expiry; the web portal is often preferred for longer, more considered interactions — reviewing an agreement in detail, obtaining a formal settlement quote, or exploring refinance options.

Critically, both channels must offer feature parity and a consistent design language. A customer who begins a settlement journey on the web and resumes it on their mobile device should experience seamless continuity, not frustration. The best platforms are built mobile-first, ensuring that most customers who access services on a smartphone receive an experience that feels native, not compromised.

Push notifications on mobile represent a particularly powerful engagement lever. A timely, relevant notification — “Your payment has been received,” “Your annual statement is ready,” “Your agreement ends in 90 days — here are your options” — keeps customers engaged and informed without requiring them to remember to log in. This proactive stance is a hallmark of customer-centric digital strategy and a material driver of satisfaction scores.

Implementation: What Good Looks Like

A successful digital self-service channel is not delivered by technology alone. The customer experience must be underpinned by high-quality, real-time data integration with the core lending system, robust identity verification that is secure but not burdensome, and a clear content strategy that uses plain language throughout. Accessibility must be a first-class consideration, not an afterthought.

From an organisational perspective, the contact centre does not disappear, it evolves. Agents are freed from handling high-volume, low-complexity enquiries and can focus on the interactions that genuinely require human judgement: complex complaints, vulnerable customer support, and intricate end-of-term negotiations. This elevation of the agent role improves both customer outcomes and colleague satisfaction.

The Road Ahead

For automotive finance providers, the question is no longer whether to invest in digital self-service, it is how quickly and how well. The combination of portfolio growth, rising customer expectations, and the proven cost economics of digital engagement makes the case unambiguous.

A growing provider that delivers a best-in-class mobile and web self-service experience for its 150,000 in-life customers today will arrive at Year 3 with 228,000 customers who feel genuinely valued, a contact centre that has absorbed dramatic volume growth without proportional cost, and an annualised net saving of £1.2 million, alongside a measurably stronger pipeline of end-of-term refinance conversions.

In automotive finance, as in the vehicles themselves, the future belongs to those who are willing to invest in the engineering that makes the journey exceptional.